HMRC is a high-performing collection system facing a digital transformation proportion problem.

Its revenue core remains strong. In 2024–25, HMRC reported total tax revenues of £875.9 billion, the highest on record for the fourth successive year, and estimated that its compliance activities produced £48.0 billion in yield, up 14.9% from 2023–24 and £2.6 billion above target. Those figures come from the National Audit Office’s review of HMRC’s 2024–25 accounts.

The pressure appears at the service edge, where digital migration, Making Tax Digital, app adoption, agent dependence and complex taxpayer support are raising Activation Load faster than HMRC can interpret and correct the consequences.

The centre of the system continues to function. Pressure appears in the human-resolution side, where taxpayers, agents and small businesses need explanation, correction, reassurance and a clear route through complexity.

Gross HMRC tax and National Insurance receipts for April 2025 to March 2026 were £938.8 billion, £80.2 billion higher than the same period a year earlier, according to HMRC’s monthly tax receipts bulletin. That figure needs careful handling: it’s cash-basis monthly receipts data and remains provisional until aligned with HMRC’s Annual Report and Accounts.

The Continuum diagnosis is proportion loss at the edge.

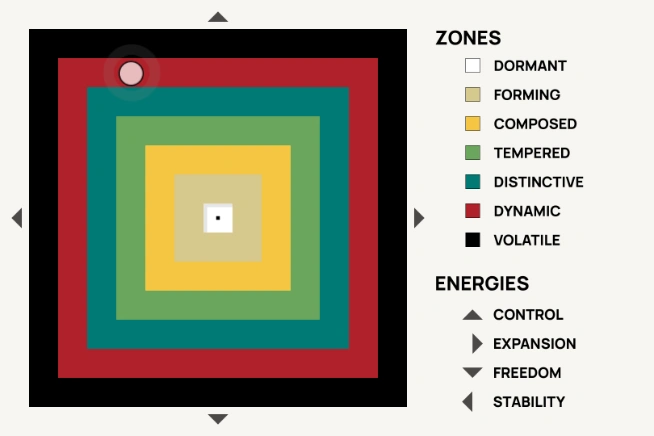

HMRC has a Composed / Tempered collection core and a Dynamic service edge.

Origin and inheritance

HMRC was created as machinery of state before it was expected to behave like a modern service brand. It inherited authority, enforcement, inspection, customs and collection functions.

The Commissioners for Revenue and Customs Act 2005 became law on 7 April 2005 and created HMRC by integrating the Inland Revenue and HM Customs and Excise. HMRC’s own internal manual describes this institutional transition in its note on the integration of the two former departments.

That origin still shapes the organisation.

Its own public description says it’s the UK’s tax, payments and customs authority, responsible for collecting money that pays for public services, providing targeted financial support, and making it hard for the dishonest minority to cheat the system. That purpose is set out on HMRC’s official organisation page.

This makes HMRC a Control institution by design. It sets obligations. It applies rules. It defines deadlines. It protects the tax base. Those behaviours belong to the basic function of a tax authority.

The Expression challenge is the balance between Ruler and Navigator. HMRC needs both. Ruler says: comply, submit, pay. Navigator says: here’s the route, here’s the next step, here’s how to get it right.

At present, HMRC is easier to experience as Ruler than Navigator.

Continuum position

Dormant is a poor fit for HMRC’s primary diagnosis. The organisation has high activation, deep repetition, extensive data and national behavioural reach.

Volatile is premature as a current diagnosis. Containment remains intact. Revenue still arrives. Authority still functions. The system can still act.

The most precise diagnosis is:

Composed / Tempered collection core. Dynamic service edge. MTD increasing Activation Load.

HMRC’s strategic objectives include closing the tax gap, improving day-to-day performance and customer experience, modernising tax and customs administration, building a skilled and engaged workforce, and supporting wider government economic aims. The National Audit Office summarises these objectives in its report on HMRC’s 2024–25 accounts.

The collection core has the features of a Composed system: repeatable behaviour, clear rhythms, data, targets and institutional memory. PAYE, Self Assessment, VAT, compliance yield, tax-gap measurement and debt management all generate regular behavioural evidence.

The service edge is closer to Dynamic. Activation has risen faster than interpretation. More obligations are being placed on taxpayers. More journeys are being pushed into digital channels. More complex queries are being routed through thin support structures. Agent frustration is becoming a structural signal rather than background irritation.

The proportion problem

Proportion is the survival discipline that keeps scale within the limits of understanding.

For HMRC, the central question is whether the organisation can feel the consequences of its own behaviour quickly enough, interpret those consequences honestly enough, and act before trust weakens.

The National Audit Office reported that customers accessed online Personal Tax Accounts, Business Tax Accounts and the HMRC app 199 million times in 2022–23, up from 62 million in 2016–17. In the same year, HMRC also received 22 million items of correspondence and 38 million telephone calls from customers. Both figures appear in the NAO’s report on customer service at HMRC.

Those two facts belong together.

Digital usage has grown sharply, while the need for human resolution remains stubbornly present. That’s the core proportion problem. Digital activation can rise while human complexity keeps reporting back through calls, correspondence and agent pressure.

Behavioural read

HMRC rewards collection, compliance yield, automation, standardisation, risk scoring, digital usage and target-driven throughput.

It protects the tax base. It protects statutory authority. It protects the assumption that most people will comply if the system is visible, credible and backed by consequence.

Its difficulty appears when the taxpayer leaves the standard route.

A routine PAYE interaction can be Composed. A simple app task can be Tempered. But a disputed tax code, unresolved correspondence, a delayed repayment, an agent chasing a case, or a landlord preparing for Making Tax Digital can push the same institution into Dynamic pressure.

The NAO found that HMRC’s telephone and correspondence performance had been below expected levels for almost all of the previous five years. It also reported that HMRC estimated 72% of customer calls in 2023–24 were caused by “failure demand”, including HMRC process failures or delays, customers chasing progress, and customer errors. This is set out in the NAO’s report on HMRC customer service.

The system is creating demand through its own difficulty completing work cleanly. That creates both operational cost and behavioural leakage.

Proof system

HMRC’s strongest proof is revenue. Its second proof is compliance yield. Its third proof is digital adoption.

The UK tax gap in 2023–24 was estimated at 5.3% of total theoretical tax liabilities, or £46.8 billion, meaning HMRC collected 94.7% of all tax due. The Corporation Tax gap increased to 15.8% and represented 40% of the overall tax gap by tax type. Small businesses accounted for 60% of the tax gap by customer group. These figures come from HMRC’s Measuring Tax Gaps summary.

HMRC’s digital proof is also real. In 2025, HMRC said its app had more than 136 million logins, a 20% increase on 2024. Total annual users passed 7.18 million, up from 5.09 million, and app downloads exceeded 4.2 million. The figures appear in HMRC’s GOV.UK release on increased use of the HMRC app. One caveat is important: the 2025 data covered 1 January to 30 November, while the 2024 comparator covered the full calendar year.

The digital story is strong, with a clear caveat around the comparison period.

The control proof is more exposed. The Comptroller and Auditor General qualified HMRC’s 2024–25 Resource Accounts because of material levels of error and fraud in Corporation Tax R\&D reliefs, Personal Tax Credits and Child Benefit. That qualification is covered in the NAO’s report on HMRC’s 2024–25 accounts.

The proof system divides into five layers.

- Money proof is strong.

- Digital proof is strengthening.

- Service proof is strained.

- Trust proof is weakening.

- Control proof is uneven in specific expenditure areas.

This creates exposure if an abrupt shock makes the unevenness visible at scale.

Energy and Expression

HMRC’s leading Energies are Control and Stability.

Control gives the system authority, precision, judgement, boundaries, rules and standards. Stability gives it repetition, continuity, predictable routines and a sense of administrative permanence. Together, they explain why HMRC can operate at national scale. They also explain why the system can become rigid under pressure.

The practical challenge is the balance between Ruler and Navigator. Ruler sets the rule. Navigator makes the route legible.

The Public Accounts Committee said HMRC’s digital services are best suited to straightforward queries and can’t always replace traditional channels. That judgement appears in the PAC’s report on HMRC customer service and accounts 2023–24.

HMRC can set obligations digitally, but it can’t treat every digital route as a substitute for judgement, reassurance and exception handling.

The Stability layer reinforces the same risk. Rules, routines and published standards create trust when people can follow them. Under Dynamic pressure, they can also make the system feel stiff, slow and hard to correct.

HMRC needs more Navigator inside its Control + Stability system.

Agency and communications context

HMRC’s communications context strengthens the digital transformation reading.

Industry reporting says HMRC appointed UNLIMITED & Pablo as its creative agency partner in May 2022, after a Crown Commercial Service pitch process. The appointment covered strategic and creative brand work, including campaigns such as Self Assessment and Tax Credits. HMRC’s Jennifer Hepker, then Head of Brand & Campaigns, said the agency team had shown creative credentials, behaviour-change understanding and a collaborative approach. UNLIMITED’s Tim Bonnet framed the work around supporting HMRC’s move towards a more customer-centred and modern service. Sources: MarComm News and LBB.

In 2025, HMRC reappointed UNLIMITED & Pablo as lead creative partner. Industry reporting said the contract was worth £14 million, running initially for three years with an option for an additional year. The same coverage described the work as supporting HMRC’s digital transformation and helping move HMRC away from the older “Tax Man” persona towards a more human and supportive service identity. Source: LBB.

This agency context is useful because the communications task matches the wider Continuum diagnosis. HMRC is trying to encourage digital self-service and make routine tax behaviour feel easier, while the operational evidence shows pressure at the human-resolution side. Campaigns can move simple behaviour into digital channels. They can’t by themselves solve unresolved correspondence, long waits, agent frustration or failure demand.

The clearest campaign example is “You’re On It”, launched in 2024 by Pablo & UNLIMITED to promote HMRC’s digital services and encourage people to use online tools and the HMRC app for simple tasks rather than calling or writing. Campaign coverage names Harriet Knight, Managing Director at Pablo London, and Tim Snape, Executive Creative Director at Pablo, among the public agency-side voices explaining the work. HMRC-side coverage also quotes Neil Martin, Deputy Director of Strategic Communications, Campaigns and Marketing, on the aim of making interactions quicker and easier through online services. Source: MarComm News. Additional campaign analysis is available from Creative Salon.

The campaign expression is significant. “You’re On It” does not present HMRC mainly as an enforcer. It tries to make digital tax behaviour feel light, simple and manageable. That is Navigator behaviour: helping people find the route through the system. The risk is that the creative promise can only travel as far as the service reality allows. If taxpayers are asked to move online for simple tasks but still cannot resolve complex cases, the brand experience splits.

A later phase of the app campaign broadened the digital push. Creative Salon reported in 2025 that TMW, part of Accenture Song, and Pablo launched a second major HMRC campaign using surreal humour to promote the app to adults aged 18 to 65. That campaign was described as part of a broader digital transformation programme to help HMRC become a trusted, modern tax and customs service. Source: Creative Salon.

HMRC’s “Tax Confident” campaign adds a different note. Launched in March 2026, it’s described by HMRC as an educational campaign resource designed to help people understand tax through simple explanations, videos and examples. The campaign is aimed partly at people setting up new small businesses and people thinking about retirement. Source: GOV.UK. The campaign site describes its purpose as giving people a clear picture of how tax works, without jargon or complicated numbers. Source: Tax Confident.

That makes “Tax Confident” a stronger Navigator asset than the app advertising. It is about comprehension, not only channel migration. In Continuum terms, it works closer to Interpretive Capacity: helping people understand what the system is asking of them before pressure builds.

HMRC also has a more deterrent communications history. “Tax avoidance: don’t get caught out” warns people about avoidance schemes and bad tax advice, using personal stories and direct consequence language. Source: Don’t Get Caught Out. GOV.UK says HMRC and the Advertising Standards Authority launched action in 2020 to disrupt promoters of tax avoidance schemes. Source: GOV.UK.

This shows the Ruler / Navigator mix in communications. HMRC warns people about risk, then offers a safer route. That behaviour is legitimate for a tax authority. The strategic question is whether the same clarity exists at the service edge, where people need movement through a real case rather than awareness of a campaign.

Making Tax Digital itself appears to be managed as an HMRC-led government transformation programme rather than an agency-led communications project. HMRC’s organisation chart lists Craig Ogilvie as Director of the Making Tax Digital Programme. Source: HMRC organisation chart. HMRC’s updated Accounting Officer’s Assessment says the programme has a dual Senior Responsible Owner structure, with Suzanne Newton and Jonathan Athow appointed, and that it is governed principally through the MTD Programme Board, reporting to HMRC’s Executive Committee and the Reform and Modernisation Committee. Source: MTD Accounting Officer’s Assessment.

This distinction is important for strategists. Agencies can support behaviour change, channel migration and public confidence, but the transformation itself belongs to HMRC. The communications layer can make digital adoption feel easier. The programme layer must make digital adoption work when users hit complexity.

The strategic implication is clear: HMRC’s agency work is aligned with digital transformation, but the bigger task is proportion. Communications should not simply increase digital uptake. It should help separate routine digital behaviour from the cases that need guidance, correction, exception handling or controlled Freedom. The useful communications role is to strengthen Navigator behaviour while avoiding extra Activation Load at the service edge.

Distinctive assets

HMRC’s first distinctive asset is legal authority. It can require action. It can investigate. It can assess. It can penalise.

Its second asset is PAYE. PAYE makes tax behaviour almost invisible for millions of employees. It turns compliance into deduction before choice.

Its third asset is national reach. HMRC touches individuals, employers, landlords, sole traders, companies, agents, payroll teams and software providers.

Its fourth asset is data. HMRC sees patterns across income, business activity, employment, VAT, benefits, property and debt.

Its fifth asset is the app and digital account infrastructure.

Its sixth asset is the agent community. This may be the most under-valued asset in the system.

In HMRC’s 2024 customer survey, 68% of small businesses and 66% of mid-sized businesses reported a good overall experience of HMRC, while only 33% of agents did. The same survey identified three strong influences on agents’ overall experience: how well HMRC resolved issues, the acceptability of time taken to reach an end-result, and how good HMRC was at getting tax transactions right. These findings appear in HMRC’s Agents, Small and Mid-Sized Businesses Customer Survey 2024.

Agents are the system’s external Interpretive Capacity.

They absorb complexity. They translate policy. They prevent errors. They reduce direct demand on HMRC. If they become more negative, HMRC loses more than goodwill.

Money engine

HMRC’s money engine is voluntary compliance.

The visible part is enforcement. The more valuable part is the enormous volume of tax paid without intervention.

The cheapest tax to collect is the tax people pay correctly because the system is clear, credible and usable. HMRC collected 94.7% of all tax due in 2023–24, based on the official tax-gap estimate.

The government is also expanding HMRC’s operational capacity. HMRC’s Transformation Roadmap says the government has provided funds to recruit and train an additional 5,500 new compliance colleagues over five years, as well as additional funding for 2,400 tax debt officers.

That may protect revenue, but enforcement is most efficient when the willing majority can comply without being forced through expensive correction loops.

HMRC makes money when doing the right thing feels possible.

Value leakage

Value leaks when taxpayers try to comply and the system can’t interpret their need. It leaks through long waits, repeated contact, unresolved correspondence and agents spending billable time chasing HMRC rather than helping clients make better decisions.

In 2023–24, HMRC answered 66.4% of customers’ attempts to speak to an adviser against a target of 85%. HMRC last met an annual telephone target in 2017–18. In 2023–24, telephone performance reached an all-time low, average call waiting times exceeded 23 minutes, and in the first 11 months of that year HMRC cut off 43,690 calls after customers had waited 70 minutes to speak to an adviser. These figures are set out in the PAC’s report on HMRC customer service and accounts 2023–24.

These service metrics are trust events. They tell taxpayers and agents whether the institution will remain reachable when the standard journey fails.

Central tension

The central tension is Ruler / Navigator under Dynamic pressure, intensified by Stability.

HMRC has to be Ruler. It can’t abandon authority. It can’t make tax feel optional. When Ruler expression rises without enough Navigator support, Control starts to feel coercive.

The Public Accounts Committee said it was concerned HMRC had sought to degrade its telephone service to drive taxpayers to digital channels. It also said HMRC’s treatment of taxpayers had damaged trust in the tax system. This is PAC’s assessment and should be presented as such, not as proven intent. The wording appears in the PAC’s report on HMRC customer service and accounts 2023–24.

Even if HMRC disputes the intent, the perception carries risk. If digital transformation is experienced as forced channel withdrawal rather than better service, adoption starts to feel like coercion.

Stability adds a second layer of tension. HMRC depends on repeated rhythms: tax years, deadlines, returns, thresholds, payment dates, letters, guidance and service standards. Those rhythms create confidence when they reduce doubt. They create frustration when they add friction without resolution.

Control without enough Navigator creates pressure. Stability without enough correction creates system debt.

Making Tax Digital as planned Activation Load

Making Tax Digital is a major increase in Activation Load. MTD for Income Tax becomes mandatory in phases: qualifying income over £50,000 from 6 April 2026, over £30,000 from 6 April 2027, and over £20,000 from 6 April 2028. The timetable is set out in GOV.UK guidance on when taxpayers need to use Making Tax Digital for Income Tax.

The £20,000 threshold change is expected to bring approximately 970,000 additional individuals into scope. Those within scope must keep digital records and use MTD-compatible software to send quarterly updates and an end-of-year tax return. These details are set out in the government’s policy paper on reducing the MTD for Income Tax threshold from £30,000 to £20,000 from April 2028.

GOV.UK also states that taxpayers may be exempt from MTD for Income Tax if they’re digitally excluded. This appears in the same guidance on MTD for Income Tax requirements and exemptions.

MTD is planned Activation Load. A separate shock would be an abrupt event, such as a system failure or public crisis, that exceeds HMRC’s absorption capacity at the time.

A large reform can be absorbed by a system with strong sensing, interpretation and correction. A system already in Dynamic pressure has less room.

The MTD risk path is easy to trace. More taxpayers enter the regime. Software, record-keeping or guidance creates resistance. Agents absorb the first wave, and HMRC contact rises. Resolution capacity lags, and public stories become simple and damaging. Political pressure rises, and HMRC responds reactively. Trust falls, and Dynamic becomes Volatile.

Current condition

HMRC needs a mixed-zone diagnosis because the evidence doesn’t describe one uniform system.

The collection core is repeatable, data-rich and high-yield. PAYE, receipts, compliance yield, tax-gap measurement, app use and debt recovery all show regular feedback, operational memory and the ability to act. That part of the system behaves closest to Composed / Tempered.

The service edge is Dynamic. Activation is rising through digital migration, Making Tax Digital, agent dependence and complex taxpayer contact, while the correction layer struggles with failure demand, call access, correspondence and visible resolution.

The current condition is:

Composed / Tempered collection core. Dynamic service edge. Control + Stability under pressure. Missing Freedom as stabiliser. Planned MTD load increasing Volatile oscillation risk.

HMRC is strongest where behaviour is automated, repeated and measurable. It is most exposed where taxpayers and agents need interpretation, movement and repair.

The risk is that ordinary Dynamic oscillation carries the service edge into Volatile conditions: reactive decisions, unstable promises, contradictory evidence and faster trust loss.

The Energy pattern is now clearer:

Control 50%. Stability 40%. Expansion 10%. Freedom 0%.

HMRC is dominated by authority and routine. It has some expansion through digital migration and MTD, but very little release, flexibility or user agency. This gives the system strength at scale and creates difficulty when people need movement, explanation or exception handling.

Volatile risk

Volatile begins when containment fails.

For HMRC, containment failure would not necessarily mean tax collection stops overnight. Public systems rarely fail like a light switch. It would mean evidence starts contradicting itself in public, decisions become reactive, promises become unstable, and trust falls faster than HMRC can repair it.

The likely triggers are MTD overload, a major digital failure near a deadline, a visible case of vulnerable taxpayers being unable to get help, professional-body frustration becoming organised political pressure, another fraud/error story, or service failure during a high-volume period.

The Control + Stability pattern creates a specific Volatile route. The system can respond to pressure by adding more rules, more process, more deflection and more measurement. That can make the organisation look more serious while increasing the load on taxpayers, agents and staff.

The risk is power and routine outrunning comprehension at the point where people need help.

Strategic task

The strategic task is to restore proportion at the human-resolution layer. This means reducing avoidable contact by fixing causes, treating agents as operating infrastructure, giving complex cases a visible path, and making MTD support feel like Navigator behaviour before Ruler behaviour appears.

It also means using app and digital accounts for simple, repeatable tasks, while protecting human judgement where anxiety, ambiguity and financial consequence are highest.

It means making Stability useful. Repetition should reduce doubt. Standards should support action. Routines should remove friction. When Stability becomes paperwork without resolution, it adds weight to the system.

And it means measuring comprehension, not just activity: not only logins, calls answered, letters sent and yield secured, but whether people understood what to do next.

That is the move toward Tempered.

HMRC needs proportionate Control + Stability: authority expressed through clear routes, reliable correction, practical guidance and visible service recovery.

Verdict

HMRC is a Control + Stability institution with a strong revenue core and a service edge moving through Dynamic pressure.

Its Ruler expression is clear. Its Navigator expression needs strengthening. Its missing stabiliser is controlled Freedom.

That Freedom should not weaken authority or make compliance feel optional. It should create release inside the system: clearer routes out of stuck cases, fewer unnecessary permission steps, easier correction, practical exemptions, callbacks, visible escalation and more agency for taxpayers and agents trying to comply.

Its Stability behaviours are extensive: deadlines, standards, guidance, tax years, routines and repeatable compliance systems. Those behaviours create trust when they make action easier. They create service debt when they become rigid and slow to correct.

The long-term money engine is voluntary compliance. That depends on taxpayers and agents believing that the system will help them understand, act and correct before enforcement becomes necessary.

Final diagnosis:

Composed / Tempered collection core. Dynamic service edge. Control + Stability under pressure. Missing Freedom as stabiliser. MTD increasing Activation Load. Volatile oscillation risk if Proportion not restored.

Strategic task:

Rebuild Navigator capacity and controlled Freedom inside HMRC’s Control + Stability system, so rules and routines become easier to follow, easier to correct, and less likely to trap taxpayers and agents in failure demand.

Suggested approach to the strategic task

The strategic work should begin at the service edge, where the Dynamic pressure is clearest.

Start with the moments where taxpayers and agents are already trying to comply but become stuck: unresolved correspondence, long call waits, repeated contact, MTD uncertainty, disputed tax codes, delayed repayments and unclear escalation routes. These are the points where HMRC’s Control and Stability behaviours turn from useful structure into load.

The first task is to map those moments as journeys of comprehension. For each one, ask four questions:

- What is the taxpayer or agent trying to understand?

- What does HMRC ask them to do next?

- Where does the route become unclear, slow or closed?

- What would create movement without weakening the rule?

That last question is where controlled Freedom becomes useful.

Freedom, in this context, means release inside the system: callbacks, clearer escalation, visible case status, practical exemptions, simpler correction routes, better agent access and fewer unnecessary permission steps. These are small forms of movement that reduce pressure without weakening compliance.

The second task is to strengthen Navigator behaviour. HMRC already has authority. It needs clearer routes through authority. Every major obligation, especially MTD, should be paired with visible guidance, practical examples, next-step clarity and a reliable route for exceptions.

The third task is to keep Stability proportionate. Repetition should reduce doubt. Standards should support action. Routines should make the system easier to use. When repeated processes create more contact, more delay and more chasing, Stability is being expressed under Dynamic pressure rather than Tempered discipline.

The fourth task is to measure comprehension directly. HMRC already measures activity: receipts, yield, calls, correspondence, app use, deadlines and tax-gap movement. The missing layer is whether taxpayers and agents understood what to do, completed the action successfully, and knew how to correct the situation when something went wrong.

The approach is therefore practical:

- Reduce avoidable demand.

- Strengthen Navigator pathways.

- Add controlled Freedom at stuck points.

- Lower resistance with Stability.

- Measure whether people understood and completed the next action.

That is the route back towards Tempered: authority, routine and movement working in proportion.